India is rapidly emerging as a global hub for Contract Development and Manufacturing Organizations (CDMOs), driven by a potent combination of cost advantage, regulatory credibility, and the rise of integrated, ecosystem-backed campuses. With pharmaceutical innovation decentralizing and outsourcing gaining momentum worldwide, India’s strategically designed life sciences clusters are becoming the launchpads for global pharma ambitions.

As of 2024, India’s CDMO market is estimated to be worth around USD 22.5 billion and is projected to reach USD 44.6 billion by 2029, growing at a CAGR of approximately 14.7% during this period. While figures may vary across market research firms, all point to one conclusion: India’s CDMO industry is scaling rapidly, not in isolation but as part of a broader global shift toward cost-efficient, quality-driven outsourcing.

Historically known for its cost advantage, Indian CDMOs continue to offer services at significantly lower prices than their Western or Chinese counterparts. But the real evolution lies beyond cost. Over the past decade, India has steadily built a reputation for regulatory compliance and quality excellence. As of 2024, India hosts over 650 USFDA-approved pharmaceutical manufacturing facilities—the highest number outside the United States—underscoring its ability to meet stringent international benchmarks.

However, what is powering this next wave of growth is not just affordability or compliance, but infrastructure—specifically, the emergence of ecosystem-led life sciences campuses.

Ecosystem-backed campuses are purpose-built developments within dedicated life sciences clusters that integrate research, development, and manufacturing functions in one interconnected environment. These campuses go far beyond conventional real estate—they are designed with shared infrastructure, centralized regulatory support, world-class laboratory spaces, and a built-in network of collaborators ranging from CDMOs and CROs to academia, biotech startups, and large pharma companies.

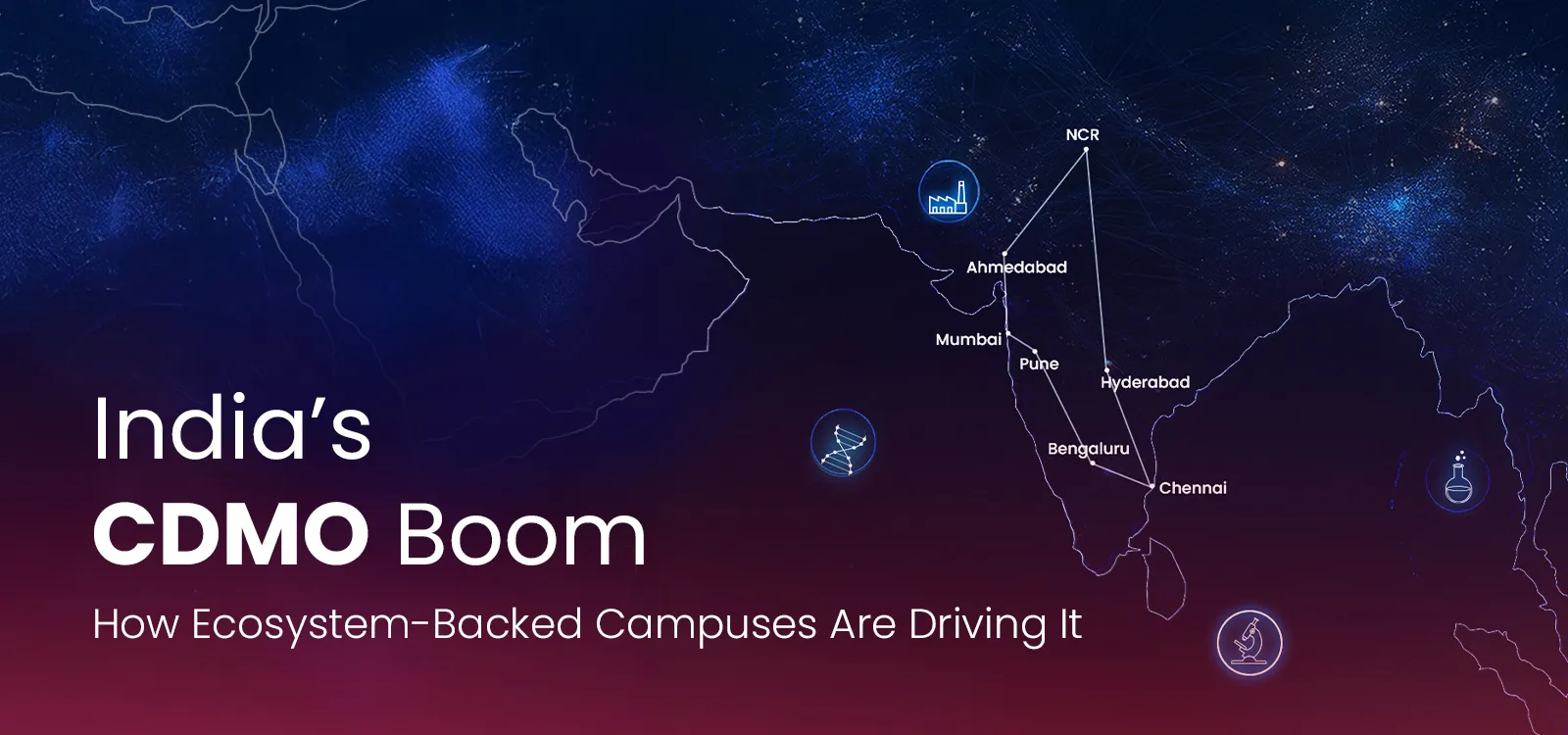

Navi Mumbai Research District (NMRD) located at the MIDC Industrial area in Navi Mumbai is a compelling example of this model. The district offers dedicated spaces for R&D labs, pilot-scale manufacturing, experience centres, and flexible offices—allowing companies to co-locate with their value-chain partners while enjoying ready access to scientific infrastructure and institutional support.

The advantage of ecosystem campuses lies in their ability to foster seamless collaboration and minimize friction across the drug development lifecycle. Co-located companies benefit from faster regulatory clearances, plug-and-play infrastructure, and access to a specialized talent pool—all of which translate into shorter development timelines and lower operational risk. These environments are designed for agility and scale, helping companies focus on science instead of setup.

In contrast, standalone facilities—often located in industrial zones without sectoral focus—can face prolonged approval timelines, fragmented supply chains, and higher capital expenditure. Without proximity to service partners, equipment providers, or regulators, standalone units are less adaptive in a landscape where speed, compliance, and technical complexity are non-negotiable.

The growing prominence of such ecosystems is reflected in the scale of investment pouring into them. In Genome Valley, a leading life sciences cluster near Hyderabad, European pharma company KRKA and Indian player Laurus Labs announced a ₹2,000 crore joint investment to set up pharmaceutical and biopharmaceutical manufacturing facilities. Laurus Labs has also inaugurated a state-of-the-art R&D centre in the same cluster, with an additional investment of ₹250 crore.

Aragen Life Sciences, located in the Uppal–Nacharam cluster in Hyderabad, raised USD 100 million from Quadria Capital in January 2025, valuing the company at around USD 1.2 billion. Meanwhile, global private equity firm Advent International consolidated its CDMO portfolio in India by merging Cohance Lifesciences and Suven Pharmaceuticals—signaling a strong bet on India’s ability to offer globally competitive CDMO capabilities at scale.

These investments are not just about capacity—they point toward India’s strategic repositioning as a value-added partner for global drug innovators. Increasingly, Indian CDMOs are moving into high-value segments like biologics, Highly Potent Active Pharmaceutical Ingredients (HPAPIs), Antibody-Drug Conjugates (ADCs), and cutting-edge modalities like cell and gene therapies.

According to the recent industry reports, Cell and Gene Therapies are projected to grow at a staggering CAGR of 45%, ADCs at 25%, and Nucleic Acid Therapeutics at 36%. These are the next frontiers of pharma innovation—and Indian CDMOs are investing to ensure they are part of it.

This momentum is being reinforced by enabling government policy. The Production Linked Incentive (PLI) scheme for the pharmaceutical sector, with an outlay of ₹15,000 crore, has already begun to attract large-scale investments in APIs, fermentation-based manufacturing, and high-value formulations. To further drive R&D, the Government of India approved the ₹1 lakh crore Research, Development, and Innovation (RDI) scheme in 2025. This initiative aims to incentivize private sector participation in cutting-edge innovation by offering long-term, low-interest financing to firms in sunrise and strategic sectors.

Additional policy instruments are also in play. The BioE3 (Biotechnology for Economy, Environment and Employment) policy, approved in 2024, is designed to promote high-performance biomanufacturing and transform traditional manufacturing practices with bio-based alternatives. For CDMOs operating in the biologics or biosimilar space, this is particularly relevant.

Likewise, the Promotion of Research and Innovation Program (PRIP) supports translational research and innovation-led growth across pharma and biotech, further bolstering the capabilities of organizations engaged in contract development or research services. These schemes—combined with streamlined regulatory procedures in cluster zones—are reducing project timelines and de-risking capital deployment.

Perhaps most significantly, these policy tailwinds are repositioning India not just as a low-cost manufacturing hub, but as a co-development partner for global pharmaceutical and biotech companies.

As CDMOs evolve from transactional service providers to integrated innovation partners, India’s infrastructure-first strategy is turning out to be a powerful growth engine. The future of Indian pharmaceutical manufacturing will be defined not merely by low cost or high volume—but by speed, scientific excellence, and the strength of connected ecosystems.

In today’s speed- and science-driven landscape, ecosystem-backed campuses are a strategic necessity. They are becoming essential to compete in a compliance-heavy, innovation-intensive, and rapidly evolving global market. As India continues to upgrade its capabilities and policy frameworks in tandem, the CDMO sector looks poised not just to participate in the global pharma value chain—but to lead it.